ASIA ELECTRONICS INDUSTRYYOUR WINDOW TO SMART MANUFACTURING

Global Chip Sales Surge Into 2026 on Record Momentum

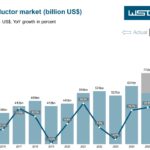

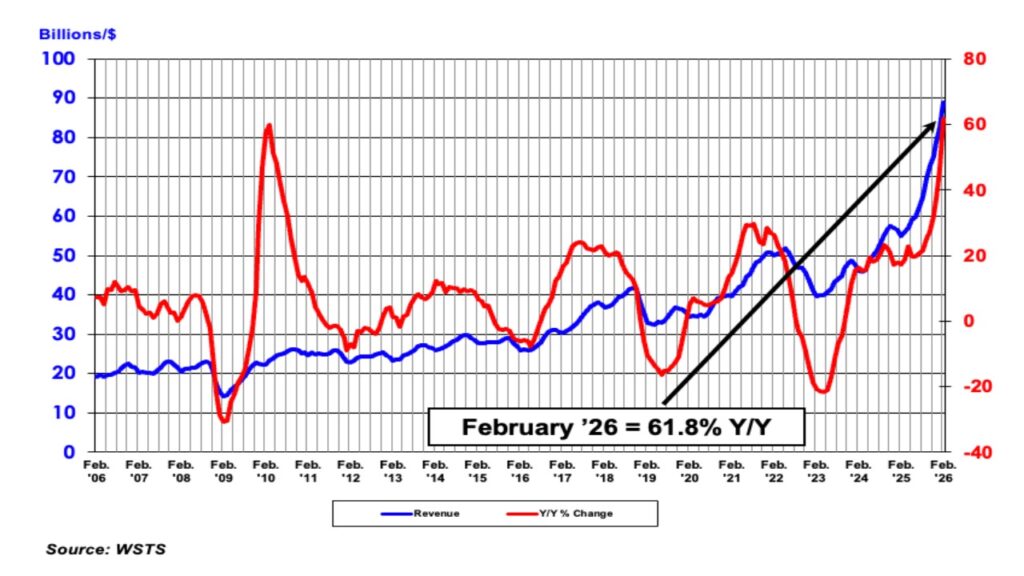

The global semiconductor industry entered 2026 at extraordinary speed, building on the momentum of its strongest year on record. The monthly global semiconductor sales report compiled by World Semiconductor Trade Statistics (WSTS) and released by Semiconductor Industry Association (SIA) showed the market hauled US$88.8 billion in February.

The February semiconductor sales is 61.8 percent more than February 2025 total of US$54.9 billion and an increase of 7.6 percent from January 2026, which posted US$82.5 billion.

Following the record-year sales of US$791.7 billion in 2025, the January and February 2026 figures reflect sustained demand across enterprise, consumer, and infrastructure markets rather than a temporary rebound. Furthermore, the latest figures also reinforce SIA’s earlier expectations that the industry will approach US$1 trillion in annual sales in 2026.

Strong Baseline

The global semiconductor sales in January 2026 of US$82.5 billion is 3.7 percent increase over December 2025 and a 46.1 percent year‑over‑year jump from January 2025. Growth was broad‑based geographically, led by Asia Pacific and China, and followed a year in which the industry achieved its highest‑ever annual revenue total.

Meanwhile, the momentum extended in February 2026 with US$88.8 billion sales climb. This sequential acceleration suggests demand strengthened beyond seasonal normalization, underscoring a structural upcycle rather than a short‑term correction.

Regionally, year-to-year sales in February were up in Asia Pacific/All Other (93.5 percent), the Americas (59.2 percent), China (57.4 percent), and Europe (42.3 percent), but declined in Japan (-0.3 percent). Month-to-month sales in January increased in the Americas (12.6 percent), Europe (10.2 percent), Asia Pacific/All Other (6.0 percent), China (3.6 percent), and Japan (3.0 percent).

“Global chip sales remained very strong in February, exceeding January’s totals and far outpacing sales from February of last year,” said John Neuffer, SIA president and CEO. “Sales into the Asia-Pacific region, the Americas, and China were all major drivers of year-to-year growth. Strong global demand is expected to persist during the remainder of the year, with annual sales projected to reach roughly US$1 trillion globally.”

Exceeds 2025 Monthly Averages

The scale of early‑2026 results becomes clearer when compared against the prior year’s performance. In 2025, global semiconductor sales reached US$791.7 billion, averaging roughly US$66 billion per month. On the other hand, January and February 2026 averaged more than US$85 billion per month, placing the industry well above its 2025 monthly pace, at least for the first two months of the year.

In fact, while December 2025 semiconductor sales closed at high US$78.9 billion, setting the bar high, but January and February 2026 managed to exceed.

This wide gap so far highlights the rapid demand, such as those for advanced logic and memory, amid the investment surges in artificial intelligence, data center, and connected infrastructure for the past years.

08 April 2026

- Share: