ASIA ELECTRONICS INDUSTRYYOUR WINDOW TO SMART MANUFACTURING

COMPUTEX 2026: Taiwan ODMs Power Global AI Shift

The year 2026 will go down in history as one of the pivotal years for the industrial-scale execution of artificial intelligence (AI) and the forthcoming COMPUTEX 2026 will serve as the definitive proof of concept for this.

As the doors of COMPUTEX 2026 open on June 2, the show floors of Nangang Exhibition Center will springboard various industry prophecies and projections, all pointing to the end of speculative hypes about AI and the onset of industrial-scale execution.

These projections did not just paint a rosy outlook of the things to come for the industry as many Taiwanese ODMs have already started to feel the vigorous market growth as translated in their recent financial reports. These and more will make this year’s edition of COMPUTEX as the inescapable center of spotlight.

Unprecedented Growths

Without a doubt, AI infrastructure is driving semiconductor market into an unprecedented growth. In its 2026 Semiconductor Outlook, U.S. market research firm IDC said the global chip market will surge to US$1.29 trillion in 2026, up 52.8 percent year-over-year from US$842.8 billion and significantly ahead of earlier market expectations.

Specifically, IDC said the memory segment is at the epicenter of this shift: DRAM revenues alone are projected to nearly triple in 2026 to US$418.6 billion, driven by demand for high-bandwidth memory (HBM) and DDR from hyperscalers and AI infrastructure providers. Meanwhile, non-memory semiconductors are growing at a robust but more measured pace, reaching US$693.5 billion in 2026.

IDC’s 2026 Semiconductor Outlook recently projected that the global industry will surge past the $1 trillion threshold, driven by a seismic 52.8% year-over-year jump in AI infrastructure spending.

Simultaneously, a separate market study by TrendForce said the move of cloud service providers (CSPs) to expand capital expenditure in AI infrastructure by 40 percent will drive an increase in global AI server shipments by 28 percent year-over-year in 2026.

Both studies highlighted significant industry transition – the training of AI models have reached a tipping point and the industry is now bracing to inferencing, or the actual deployment to billions of users.

From Macro to Micro

The single-most crucial factor in this unprecedented industry shift is the emergence of AI infrastructure and the projections made by IDC and TrendForce recently are no longer speculative forecasts. In fact, the Q1 2026 financial results of Taiwan’s leading original design manufacturers (ODMs) are the testament of AI’s industrial-scale deployment.

Revenue figures for Q1 2026 for both Tier 1 ODMs and Tier 2 specialist brands of Taiwan have skyrocketed compared to the same period in 2025.

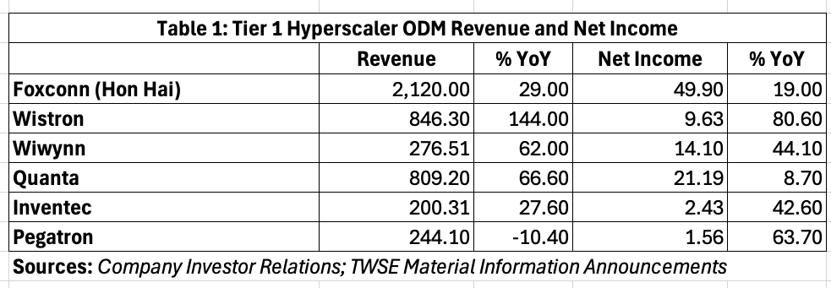

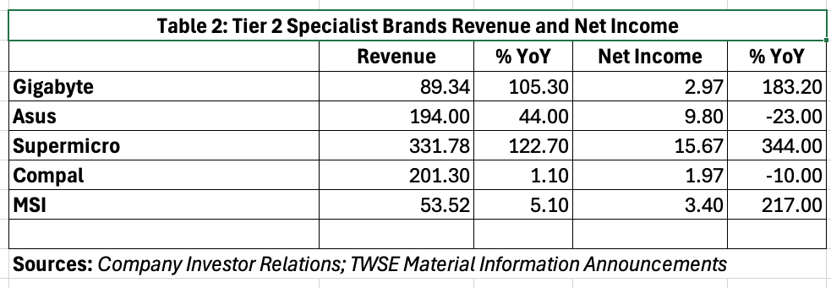

Tier 1 hyperscale ODM companies, such as that of Wistron, Foxconn, and Quanta, operate as primary partners of cloud service providers, such as Google, AWS, Meta, and Microsoft. They specialize in mass-scale, direct-to-cloud manufacturing. Meanwhile, Tier 2 specialist brands are enterprise-grade solution providers and channel brands, like ASUS, Gigabyte, and Supermicro. They translate AI power for enterprises and governments that require specialized and localized hardware.

In Tier 1 ODMs (Table 1), Wistron was the run-away winner jumping 144 percent YoY to NT$846.3 billion while other Tier 1 ODMs also managed to pull through a double-digit growth rate except for Pegatron.

In general, Tier 1 companies’ growth is attributed primarily from the robust demand for AI computing power as the primary driver of the next-wave server growth. This explains of the three-digit growth of Wistron, which transformed from legal PC assembly to becoming a provider of high-value AI baseboards.

Just like Tier 1 companies, Tier 2 specialist brands also saw dramatic increase in revenues (Table 2) for Q1 2026 led by Supermicro, which grew 123 percent YoY to NT$331.78 billion. Incidentally, Supermicro’s net income for the same period grew at a historic 344 percent year-on-year to NT$15.67 billion.

The company has stirred strategic dominance in the AI hardware market and has made strategic tie-ups with chipmakers such as NVIDIA. It has also ventured strongly on liquid cooling solutions.

Same-tier companies Q1 2026 revenues also managed to register double-digit growth rate such as Gigabyte (62.7 percent) and Asus (44 percent).

Increasing Capex

According to IDC, hyperscale capital expenditure exceeded US$100 billion for the first time in Q3 2025, and this is expected to increase capex by 70 percent year over year to approximately US$600 billion in 2026.

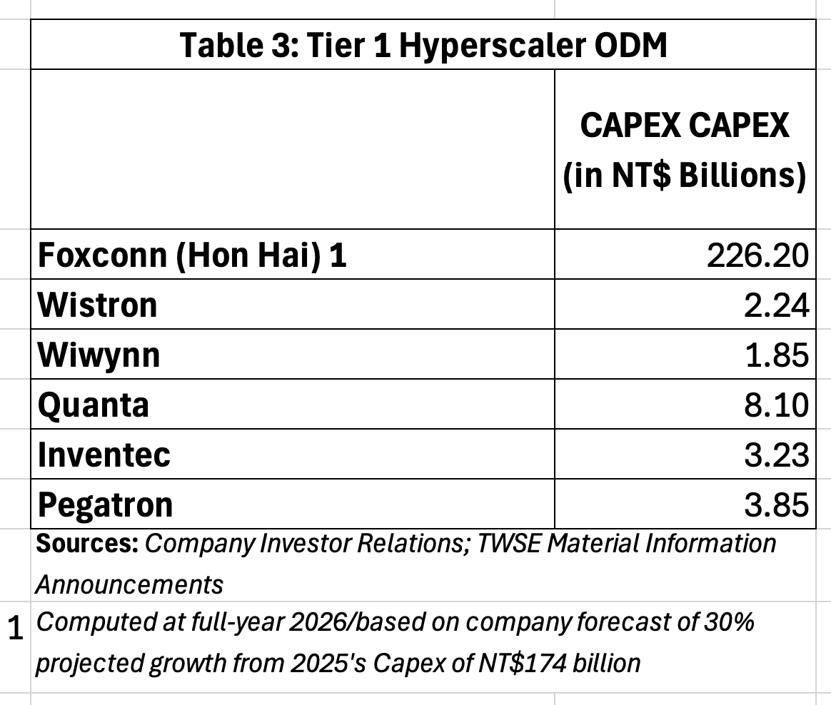

To catch up with the robust demand growth, Taiwanese companies have also expanded their capital expenditure not just to meet AI server shipments and chip capacities, but also the liquid cooling systems. As AI chips move from training to inference, the industry expects 100kW chips to generate enough heat that could not be sustained by traditional air-cooled systems.

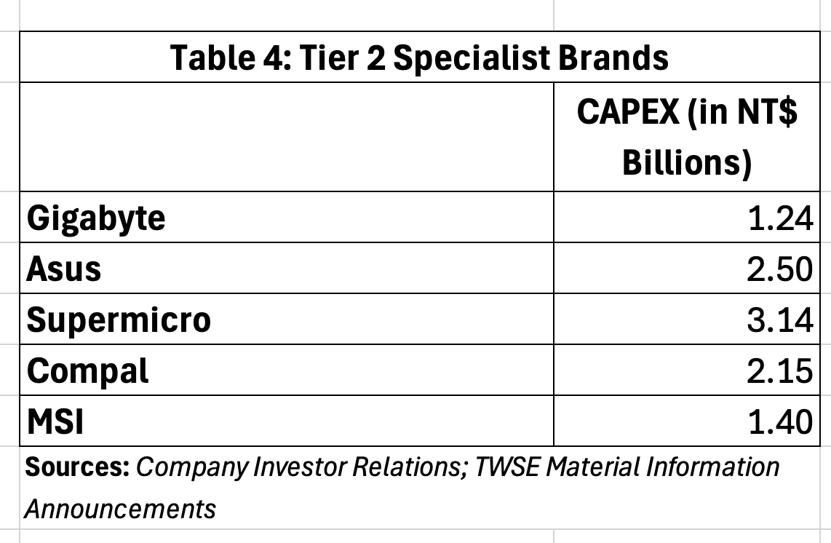

For this reason, both Tier 1 and Tier 2 Taiwanese companies are upping the ante for its capital expenditure (Tables 3, 4). Foxconn said it has allocated NT$226.20 billion for the entire 2026, up 30 percent from previous year. All companies in Tier 1 have also allocated sizeable amount of capital expenditure for Q1 2026.

Meanwhile, Tier 2 companies have also increased their respective capital expenditure such as Supermicro, which allocated NT$3.14 billion in Q1 2026 alone.

The Bottom Line for Computex 2026

While geopolitical tensions and supply chain bottlenecks continue to pose caution on the industry in general, the financial health of Taiwan’s Tier 1 and Tier 2 players is unprecedented.

As COMPUTEX 2026 opened its doors on June 2, one can say without a doubt that global AI market has moved beyond experimentation stage to industrial-scale execution. The critical players of the AI era have shown market forecasts are coming true just by looking at their Q1 2026 financial data and they are all in Nangang Exhibition Center in Taipei to show the world how they did it.

02 June 2026

- Share: