ASIA ELECTRONICS INDUSTRYYOUR WINDOW TO SMART MANUFACTURING

SEMI: AI Boom to Fuel Memory Fab Spending Past US$50B

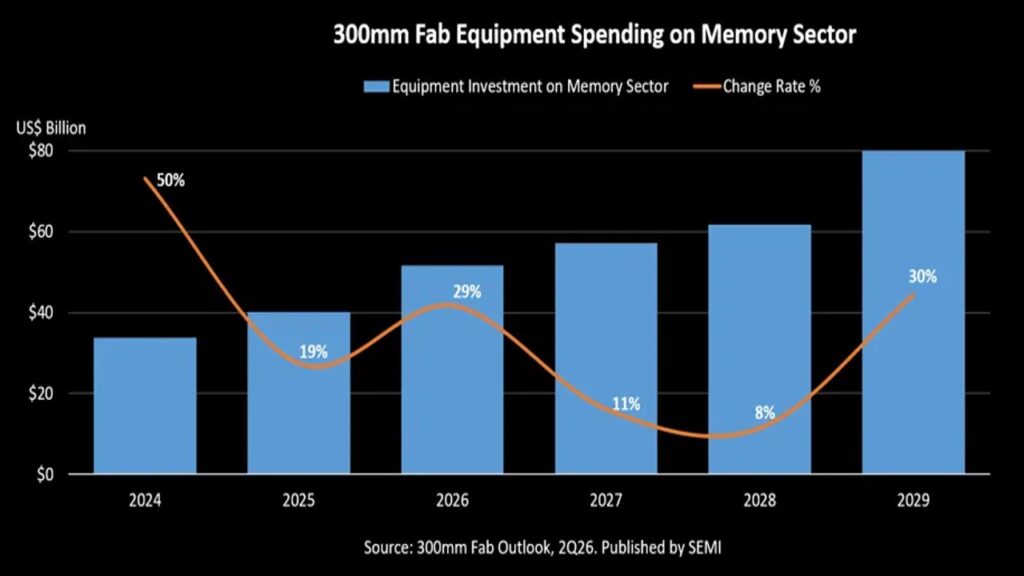

Global investment in 300mm wafer fabrication equipment for the memory sector is set to cross a historic threshold in 2026, fueled by surging demand for artificial intelligence (AI) applications.

According to SEMI’s latest 300mm Fab Outlook, spending is forecast to rise 29 percent year over year to US$52 billion, before climbing another 11 percent to reach US$57 billion in 2027.

This growth underscores accelerating capital deployment across the semiconductor ecosystem as hyperscalers, data centers, and advanced computing platforms expand to support increasingly data-intensive workloads.

AI Infrastructure Spurs Capacity Expansion

The sharp uptick in investment reflects rising demand for high-performance memory, particularly for AI workloads. Industry capacity is also expected to increase, with global 300mm memory output projected to reach 4.1 million wafers per month in 2026 and grow further to 4.2 million wafers per month in 2027.

“Strong demand for high bandwidth memory and other advanced memory technologies is reshaping investment priorities across the semiconductor supply chain,” said Ajit Manocha, President and CEO of SEMI. “As AI infrastructure expands, memory manufacturers are accelerating investments in both capacity and technology migration to support the next wave of data-intensive applications.”

DRAM and NAND Lead Investment Growth

Spending gains are led by both DRAM and NAND segments, reflecting parallel growth in compute and storage needs. DRAM equipment investment is expected to surge 29 percent to US$37 billion in 2026, driven by strong demand for high-bandwidth memory (HBM) and DDR5 used in GPUs and AI accelerators.

Meanwhile, 3D NAND spending is projected to increase 28 percent to US$14 billion, supported by escalating storage requirements linked to AI deployments and data-heavy environments.

Technology Migration Shapes Outlook

While capacity expansion remains strong, effective output growth is tempered by increasing process complexity. Ongoing transitions to advanced-node DRAM, HBM, and higher-layer 3D NAND technologies require significant investment and longer ramp cycles.

The SEMI report tracks 413 global fabrication facilities and production lines, incorporating more than 150 updates and several new project additions since its previous release. The findings highlight continued momentum in memory infrastructure as chipmakers align investments with long-term AI demand.

30 June 2026

- Share: