ASIA ELECTRONICS INDUSTRYYOUR WINDOW TO SMART MANUFACTURING

India Braces for US$400B Electronics Peak by 2030

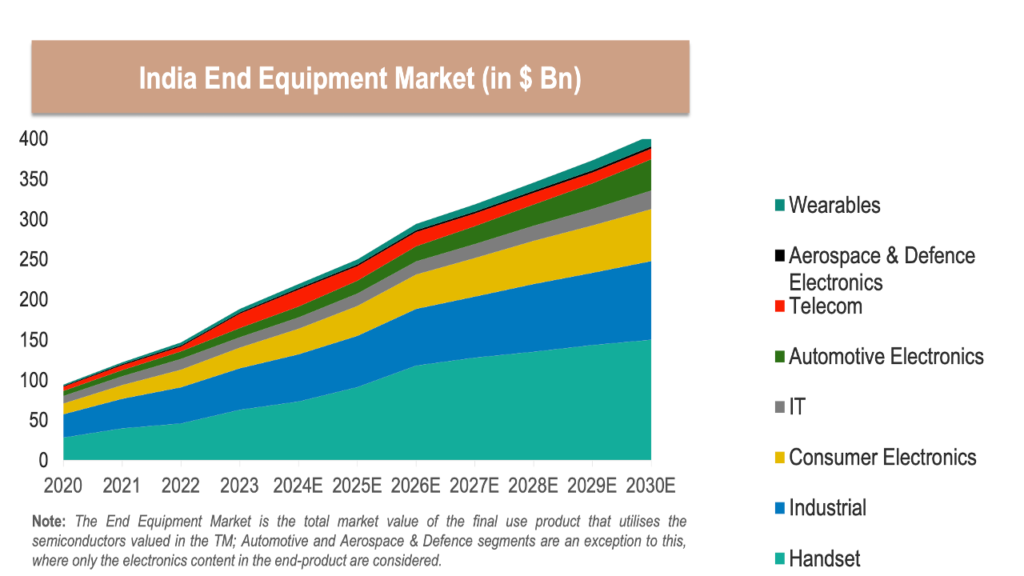

Without a doubt, the Indian semiconductor landscape is undergoing a major seismic shift. According to a recent report by the India Electronics & Semiconductor Association (IESA), the country’s electronics end-equipment market is projected to reach up to US$400 billion by 2030.

The forecast represents a massive scaleup of India from being a potential market to a dominant global electronics hub.

In an AEI interview, Ashok Chandak, President of IESA and SEMI India said the forecasted growth is fueled by a surge in domestic production and a favorable policy environment. Specifically, Chandak took note of the tremendous support poured by the central and state governments through its multitude of policies and incentives.

Chandak said Initiatives like the India Semiconductor Mission (ISM), which has already allocated nearly US$10 billion for first tranche of incentives for fab and OSAT projects, are foundational to this progress.

“Together, these steps have shifted India from a potential market to an emerging semiconductor nation,” says Mr. Chandak.

US$100 Billion Semiconductor Backbone

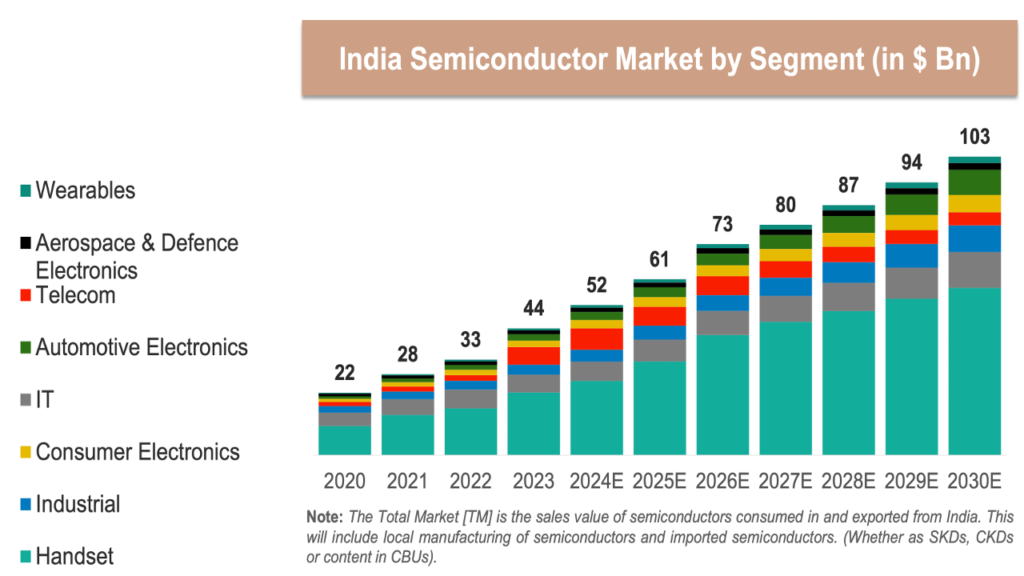

The US$400 billion surge in end-equipment market, which is the total value of finished electronics goods produced or sold in India, is powered by a rapidly maturing semiconductor ecosystem. The IESA report forecasted the India semiconductor market, which is the semiconductor components integrated into finished products, will cross the US$100 billion threshold by 2030.

As electronics manufacturing ramps up, the semiconductor intensity within these products is increasing, creating a secondary market nearly a quarter the size of the total electronics output.

The semiconductor market is currently anchored by the Handset segment, which holds a 49 percent share as of 2023, is expected to grow to 56 percent by 2030. Other sectors that will have significant pie of the country’s semiconductor market by 2030 include IT (12 percent), Industrial (9 percent), and Automotive (8 percent) electronics.

Building a Resilient Ecosystem

For fabless firms and manufacturers, the report identifies Processing (32 percent) and Memory (19 percent) as the highest value-retention segments by 2030. To capture this, IESA highlights a “Priority User Product” list for immediate localization, including RISC-V architectures for microcontrollers and GaN/SiC devices for power electronics.

However, Chandak remains pragmatic about total self-sufficiency as the country fortifies its semiconductor ecosystem. “Semiconductors have a highly globalized and complex supply chain, and no country is fully self-sufficient. India will remain dependent on the global supply chain.”

The objective, instead, is strategic autonomy—reducing vulnerability by building domestic capacity and strong competencies in selected value-chain elements.

Strategic Recommendations for Executives

To sustain this momentum, IESA advocates for a decade-long commitment to flexible policy frameworks, including:

- Semiconductor Manufacturing: Maintain financial incentives and flexible policies for the next ten years to ensure long-term growth in manufacturing and design domains;

- International Cooperations: Strengthen global partnerships to support technology sharing and collaborative growth;

- Value-Addition Targets: Linking production-linked incentive outlays to strict local value addition — 25% by 2025-26 and 40% by 2030.

- Product Creation and R&D: Consolidate multiple schemes under a unified product creation initiative;

- Supply Chain Expansion: Broadening incentives to include downstream sub-assemblies to create a holistic ecosystem;

- Workforce Development: Implement workforce development programs and collaboration with industries and universities.

06 April 2026

Cristian Canoza

- Share: